As college tuition increases nationwide, students are being forced to pay higher rates out-of-pocket, which has led to an overall increase in student debt.

About one in five households has outstanding student loan debt, according to a study by the Pew Research Center. That’s more than double the share from two decades ago and a significant rise from the 15 percent of households in 2007.

The study paints a bleak picture for households where the head is younger than 35, with 40 percent of those households having student loan debt. Household leaders between ages 35 to 44 also have a high frequency of outstanding debt at 25 percent.

English freshman Cody Thompson said he believes the percentages will quickly increase.

“I know quite a few people that have taken out some form of student loans,” Thompson said. “Every year, more students are forced to take out loans. It might not be a large amount, but it definitely is going to take a toll on people’s income once they graduate.”

According to the study, student loan debt is a problem for all income groups. The greatest portion of debt is in households in the lowest and highest fifth of the income distribution.

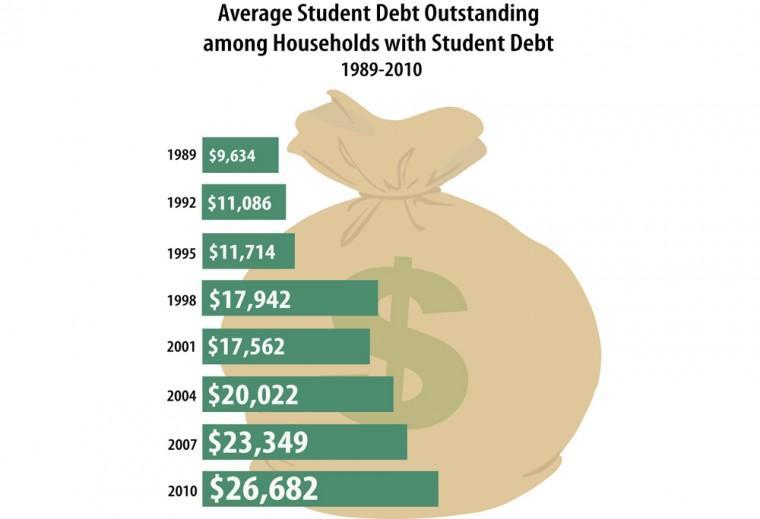

The problem isn’t just high frequency, but also the amount that graduates owe. In 2007, the average student loan debt was $23,349. The number rose to $26,682 in 2010.

Student Financial Management Center Coordinator Emily Hester said the rising amount of outstanding debt affects post-graduation budgets.

“The biggest thing is that debt takes away a piece of your budget,” Hester said. “You can’t default, even if you declare for bankruptcy. Having student loans really impacts what you can afford after graduation.”

One cause of increasing debt is the increase in tuition across the nation. At the University, residents pay $2,597 as full-time students taking 12 hours, according to the Office of Budget and Planning. Four years ago, the same students would have only paid $1,613.

Students usually have a six-month grace period after graduation before they are required to begin loan payments, but average monthly payments range from $300 to $400, Hester said. Once a student adds on rent or a cell phone payment, she said bills can become overbearing. She suggested that students make plans long before graduation and know exactly how much money they owe.

“You either have to limit expenses or increase your income,” she said. “I tell students that it is all about sacrifice and discipline. Students should take out exactly what they need. If you don’t pay, then your credit score goes down, and that can have even worse long-term effects.”