Did you know Baton Rouge is consistently one of the wettest cities in America? I’m sure you did because it rains all the time here. After about the third time I was on campus during a thunderstorm with no umbrella, I realized I’ll just have to carry one with me at all times. It’s better to constantly carry around an umbrella than occasionally be caught in a storm without it, right?

One time, while I was walking to class, wet from the rain and listening to the squish of my socks, that thought ran through my mind. This prompted me to think about how personal finance and weather are similar.

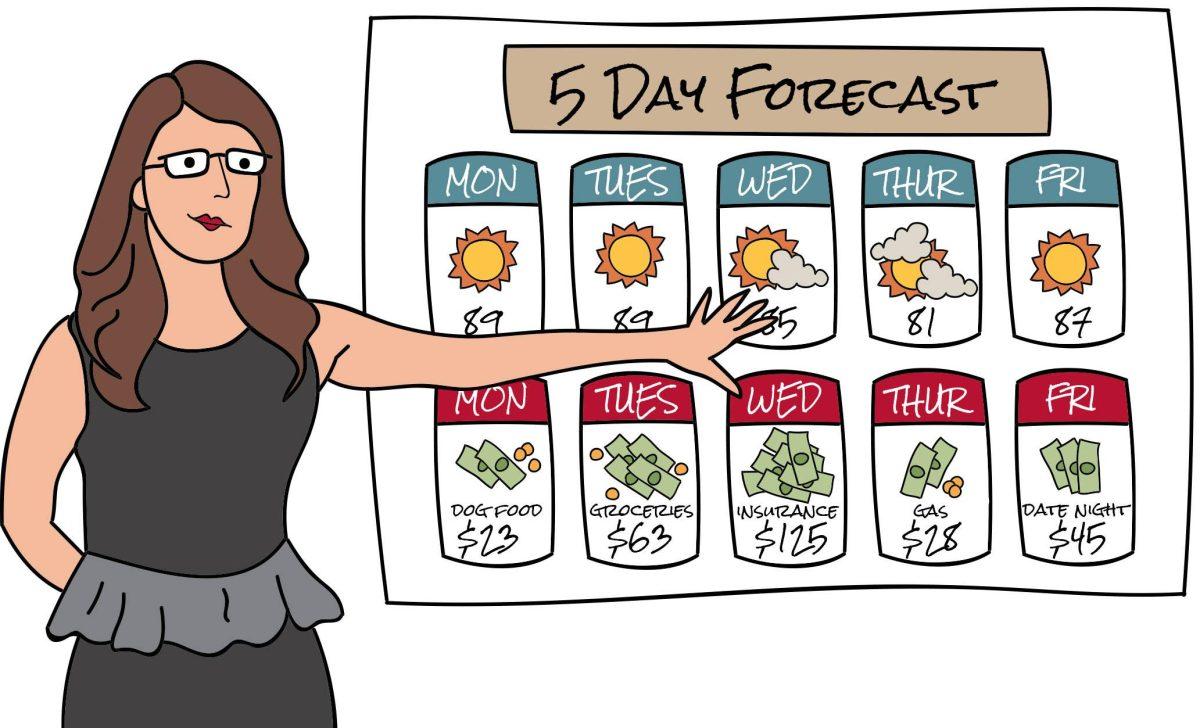

They both revolve around planning for variables that may never happen, though we constantly have warnings about them. For example, every day meteorologists update forecasts for when it will rain ranging from right now all the way to next week. What are the chances they accurately predict the chance of rain in one week’s time? If I had to guess, it’s probably a percentage lower than the number of students left in Tiger Stadium after halftime — so pretty low.

Think of meteorologists as stock experts you see on the news and read about online. A quick search on any finance website will turn up dozens of opinions ranging from the market going up 100 percent in one year to full-on doomsday coming right around the corner. It’s also a well-known fact that most expert stock pickers will not outperform the market in a given year.

Does this mean we shouldn’t listen to meteorologists and stock experts? Well, sort of. The truth is we know that in the future it will either rain or it won’t, and the stock market will either go up or go down. All the predictions, percentages and future telling are just noise that will distract you from your plans.

For example, my plan every day is to attend all my classes. If it starts raining, I’m not going to skip class, even though I would like to. Instead, I will pull out my umbrella and keep walking across campus. So if rain is not going to change my plans, there’s no reason to check the forecast before I leave. It would just be useless noise.

What I can do, however, is be aware of the worst-case scenario — rain — and then focus on what I can control to create a backup plan — carrying an umbrella.

If my financial plan is to start saving for retirement so I can retire when I’m 40 years old, I shouldn’t be concerned with trying to time the market, avoid the bad times and only invest when the market is rising. Instead, I need to lay out a plan for how to achieve my goals, focusing on what I can control.

So for my retirement plan, I should focus on how I will cut costs to save the money I’m going to be investing for retirement. I should also be aware that the worst-case scenario is a sudden large decline in the market. Much like rain, a market decline will happen and while we can speculate when it will, we won’t know until it’s too late. However, there are precautions you can take, such as hedging your investments or taking less risky investments that won’t decline as much.

Forget the forecasts and the predictions. Instead, make your plan being aware of the inherent risks associated with it and knowing how you will react when it starts to pour. It will make your life much less stressful.

Jay Cranford is a 22-year-old finance senior from St. Simons Island, Georgia.

Opinion: Planning is key in both finance and weather forecasts

November 1, 2016

Finance and Weather

More to Discover