Credit is one of those things in life that’s easy to screw up while you’re young and hard to correct when you’re older.

A few weeks ago, I wrote a column discussing how to use credit cards. I warned that improper use of a credit card can wreck your credit score and have negative consequences later in your life.

Bad credit can affect the level of living you can achieve in your life outside of college.

A bad credit score can be the difference between affording to buy your first house or having to rent a house.

Bad credit means higher interest on loans, so you may not be able to afford a car loan, and your student loan payment could be higher than the rest of your classmates.’

This is why now is a good time to learn all about credit. Because, as G.I. Joe said, “knowing is half the battle.”

Let’s start with the basics — what is credit and a credit score?

A credit score is a number used to describe your credit history. It’s a quick and easy way to tell if you will be able or trustworthy enough, to pay back debts.

The lower the number, the worse your credit.

When you have bad credit, most lenders will charge you more interest because they see you as a riskier investment. For example, landlords might not let you live in their apartment because they are afraid you will not pay them.

Luckily for you, you’ve most likely not had time to affect your credit this much, and getting bad credit is avoidable.

But before we go into how to avoid bad credit, let’s take a look at the formula used to come up with the credit score.

Keep in mind there is no one credit score the government publishes; different companies use different methods to come up with the score.

However, they are all similar, if not the same.

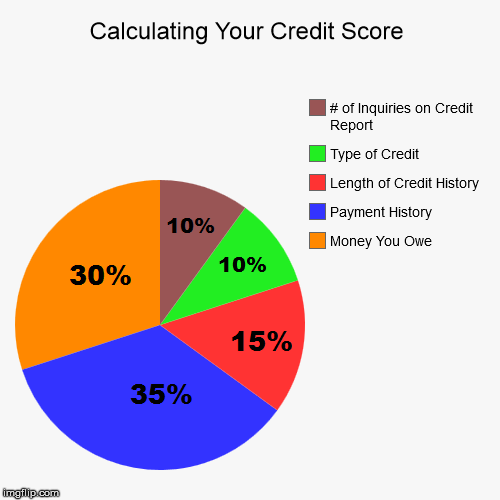

Of your entire credit score, 35 percent comes from your payment history. This is whether or not you pay your bills every month. Obviously, if you do not pay, your credit score goes down.

Another 30 percent is based on how much money you owe.

Using your credit does not automatically make your score go down. However, if you’re using the majority of your credit, other lenders might think you’re overextending your loans and won’t be able to repay everyone.

Think of this like that friend who borrows money from everyone. He may have a history of paying everyone back on time. However, if he comes asking you for money, and you know he already has borrowed from three other friends, you might think that he won’t repay you before he has paid everyone else back.

The length of your credit history makes up 15 percent of your credit score.

If someone has a longer history of credit, lenders are more comfortable loaning to them because they have more data to review.

The type of credit you have is 10 percent of your credit score.

There are different types of credit including credit cards, mortgage loans and retail accounts. This isn’t a key factor and is used in conjunction with

other elements.

For example, if you have many types of credit, but you aren’t paying them off every month, that’s bad news. However, having the same types of credit while paying your bills every month will look good.

The final 10 percent of your credit score comes from the number of inquiries on your credit report.

This shows lenders if you might be taking out credit with other people. If someone suddenly starts three new credit cards, this will look suspicious to other lenders.

One important thing to note is you usually can’t get your credit score for free.

If a service offers you a free credit score, they most likely are just giving you a free trial and will charge you eventually.

I’ll say it again to make sure you heard — your credit score is not free.

However, you can get your credit report for free.

Your credit report will have your payment history and inquires that have been made on you.

You should use these free reports to monitor your credit and dispute any unusual activity you see.

You won’t be able to see your credit score for free, but your score is calculated by the credit companies by looking at your report. Everything they see, you can see on your report.

Be sure to check your report at least once a year and dispute any suspicious charges or inquires that should not be there.

Jay Cranford is a 20-year-old finance junior from St. Simons Island, Georgia. You can reach him on Twitter @hjcranford.

Opinion: Knowledge about credit pays off in the future

March 16, 2015

More to Discover