In 1875, The American Express Company established the first company-sponsored pension in the United States. Retirement was a foreign concept at the time — most people worked until they died. Around the turn of the century, 77 percent of men over the age of 65 were still working, and those who weren’t were most likely to be disabled. However, as pensions started popping up around the nation, the number of men who retired after age 65 began to grow, reaching 42 percent by 1930.

At this point, the culture surrounding retirement began to shift. It became more acceptable for males to quit working before they died or became disabled. In fact, most private pensions at this time forced workers to retire.

Then, on Oct. 29, 1929, the stock market crashed, throwing America into the Great Depression. The sudden decline in stocks wiped out retirement plans, and the number of senior citizens living in poverty was estimated to be more than 50 percent. This prompted President Franklin D. Roosevelt to enact the Social Security Act in August 1935. Social Security would guarantee citizens approaching the retirement age of 65, the same age we still use 80 years later, would be taken care of.

After World War II thrust America into a new age of economic prosperity, the stage was set for how America would view retirement until modern day. The percent of workers with pensions would steadily rise into the ’70s, reaching a high of 55 percent in 1975.

Your great grandparents, and even some of your grandparents, lived knowing that if they put in their 40 years at the same company, they could retire at 65 with a guaranteed paycheck for the rest of their lives. If they weren’t fortunate enough to have a pension, Social Security would keep them out of poverty.

The system of pensions worked until people started living longer and costing more than companies originally accounted for. When the Great Recession of 2008 hit, many large companies lost their pensions investments, meaning they could not pay the benefits they guaranteed. Today, only around 28 percent of people in the workforce participate in an employee-sponsored pension plan.

Most baby boomers were mid-career when the Revenue Act of 1978 introduced qualified deferred compensation plans such as the 401(k). These types of retirement plans allowed for workers to save for their own retirement, which their employees would also contribute to. Many companies switched over to these types of retirement plans to save on costs and have greater flexibility.

While many baby boomers used these retirement plans, they didn’t have enough time for compound interest to take full effect. Add on the fact that many were getting ready to retire when the Great Recession hit, and most baby boomers will be retiring on the strength of Social Security payments.

The sheer number of retirees who will be taking payments from Social Security over the next couple of decades is the reason you’re hearing doomsday stories about Social Security. While it is true the government is facing problems with Social Security, we can’t be sure what it will look like when Generation X and millennials are ready to retire.

I am confident Social Security will still be around when we retire, just not in the way it exists today.

So where does that leave us? Gen X and millennials will have to take retirement into our own hands. While the generations before us were able to retire on the strengths of pensions and Social Security, we will have to retire on the strengths of our own retirement accounts and investments, such as 401(k)s and IRAs.

The good news is that millennials are saving for retirement. While studies vary, somewhere between 50 and 70 percent of millennials have started saving — and saving early, with the median age being 22. However, the bad news is that only 24 percent of millennials demonstrated basic financial literacy, according to a study by the George Washington Global Financial Literacy Excellence Center.

Because we will be the generation of do-it-yourself retirement, it is vital everyone has a basic knowledge of investments and personal finance. If not, we may see ourselves working into our 70s or 80s. Luckily for you, there are multiple resources available for you to learn about finances. There are several great TED Talks about personal finance, tons of websites and blogs by people just like you, or you can even consider taking a personal finance course here at LSU.

Jay is a 22-year-old finance senior from St. Simons

Island, Georgia.

Opinion: Millennials will be first generation responsible for retirement funding

September 14, 2016

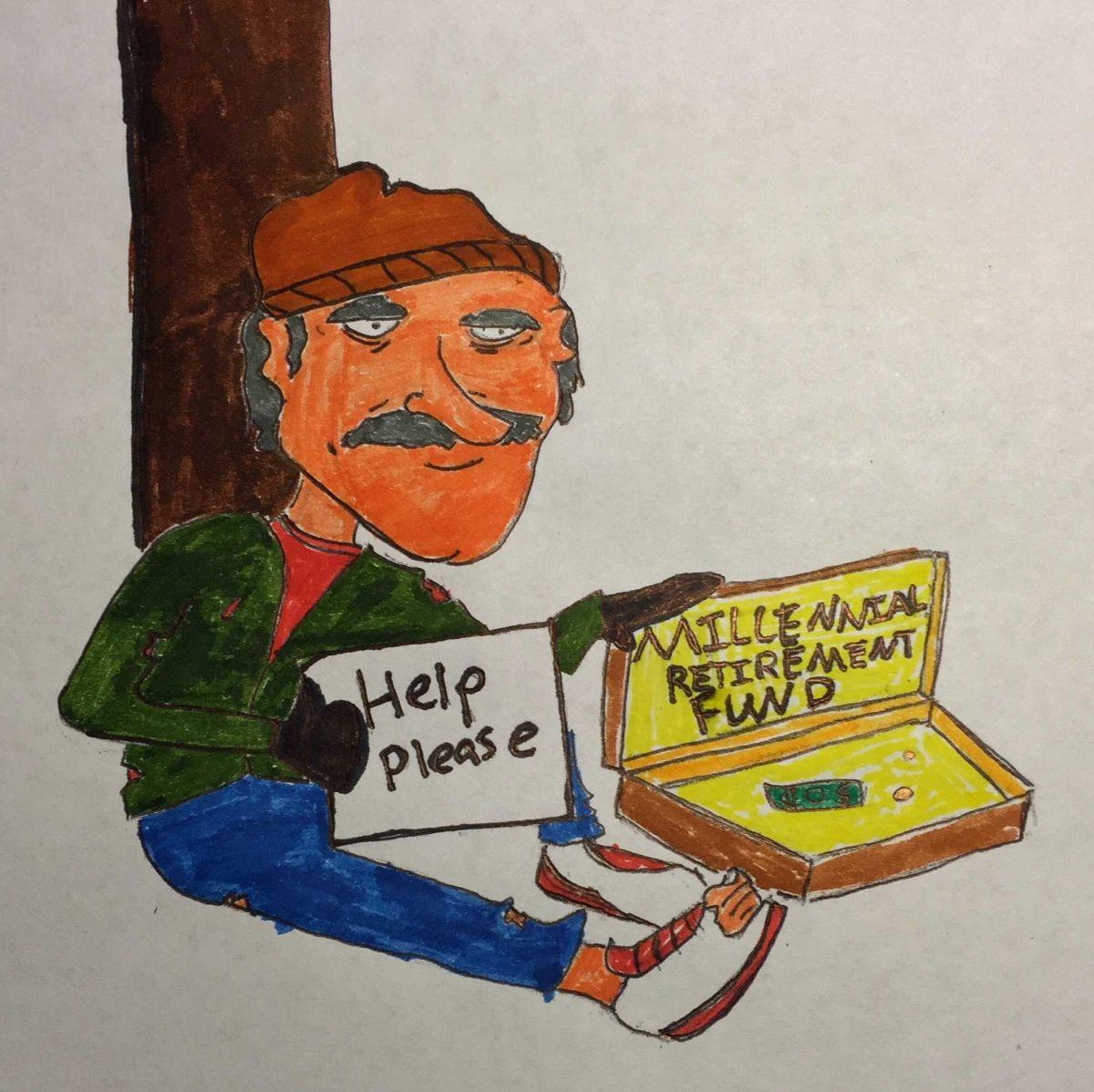

Millennial Cartoon

More to Discover